Case Study - Electric Utility Redesigns its Fixed Asset Process to Meet FERC, Leading to Better Rate Design

What do fixed assets have to do with electric rates?

Don’t underestimate the value of sound fixed asset systems in power and utility organizations. Fixed asset depreciation is a component of customer rates and the return on ratebase, which can make up to 8% of a customer’s rate. Fixed assets that were accurate can become inaccurate and a problem area due to a lack of attention to changing business processes, workforce training and succession, and lagging technology.

Here is a case study of one electric and water utilities’ recognition of problems in fixed assets and their path to a solution.

Article Takeaways

Electric Pole Construction

A large electric and water utility found that its continuing property records (fixed asset records) did not accurately reflect the actual value of the utility plant in service that served its customers.

The impact of this was to make customer rates higher than they should be due to higher depreciation expenses and return on ratebase included in customer rates.

The utility found that current business processes had not evolved with its evolution in construction and accounting processes.

The utility upgraded its financial and work order systems and used the opportunity of this change in software platforms to redesign its construction accounting business processes.

The utility also performed a full system inventory and adjusted its financial records to reflect the revised plant in service amounts.

The Situation

At one time, a large municipal electric and water utility had fixed asset records (continuing property records or CPRs) that met its needs and were considered a smooth running part of its operations and finance areas. Over time, as its workforce turned over and its technologies did not change while its construction processes evolved, the fixed asset processes became less robust. Compared to maps, GIS, and the CPR records, spot audits of the utilities’ physical plant in service showed significant discrepancies.

The impact of this was to make customer rates higher than they should be due to higher depreciation expenses and return on ratebase included in customer rates.

Issues identified

An analysis of the issues causing these discrepancies by management and a consulting firm find the following causes:

1. Inadequate and inconsistent training of field crews as the utility had relied on on the job training for crews on the business processes involved in recording CPRs.

2. Changes in construction methods led to inconsistencies in reviewing “as-builts” when construction projects were completed.

3. A seemingly too large number of CPRs, that led to mis-identification of asset types of retired fixed assets.

4. Lack of follow-up by the accounting team in recording retirements when there were misidentified fixed asset types, i.e. the accounting team did not always question obvious errors.

5. Accounting business processes did not address the changes in construction process workflows, leading to mis-identification of new assets added.

6. Accounting requested some data on forms that weren’t used for any meaningful purposes.

7. Aging software legacy systems did not allow robust reports to be run to easily identify some of these issues.

The short answer to the issues:

1. Lack of training of the teams

3. Not updating business processes for changing in the way business was being done

4. A legacy software platform that did not capture data needed to meet the utility’s needs

Electric Fixed Assets - Continuing Property Records

A solution to fix the issues

The utility wanted a solution to fix these issues now, in order to address the long-term rate impacts as they moved the utility business model into the future for providing electric and water services.

While that might sound like a lot of fluffy talk, basically, the utility recognized that providing electric service will involve new areas such as more renewable power, distributed energy resources from its customers, greater use of technology, and the impact of electric cars. For water service, greater use of technology, greater concerns on environmental impacts of water supply and the resulting changes in construction would need a better platform than the utility had now.

The utility and consultant recognize that a project like this is playing the long-game, i.e. it would take time to complete. One can’t just buy and install new software to fix the problem, there are many moving parts that are inter-related. The issues and solution rely on business process and internal controls. These are areas that sound mundane and “auditorish” but are the source and solution of many financial and operational issues in a utility as we have described here.

Designing the project

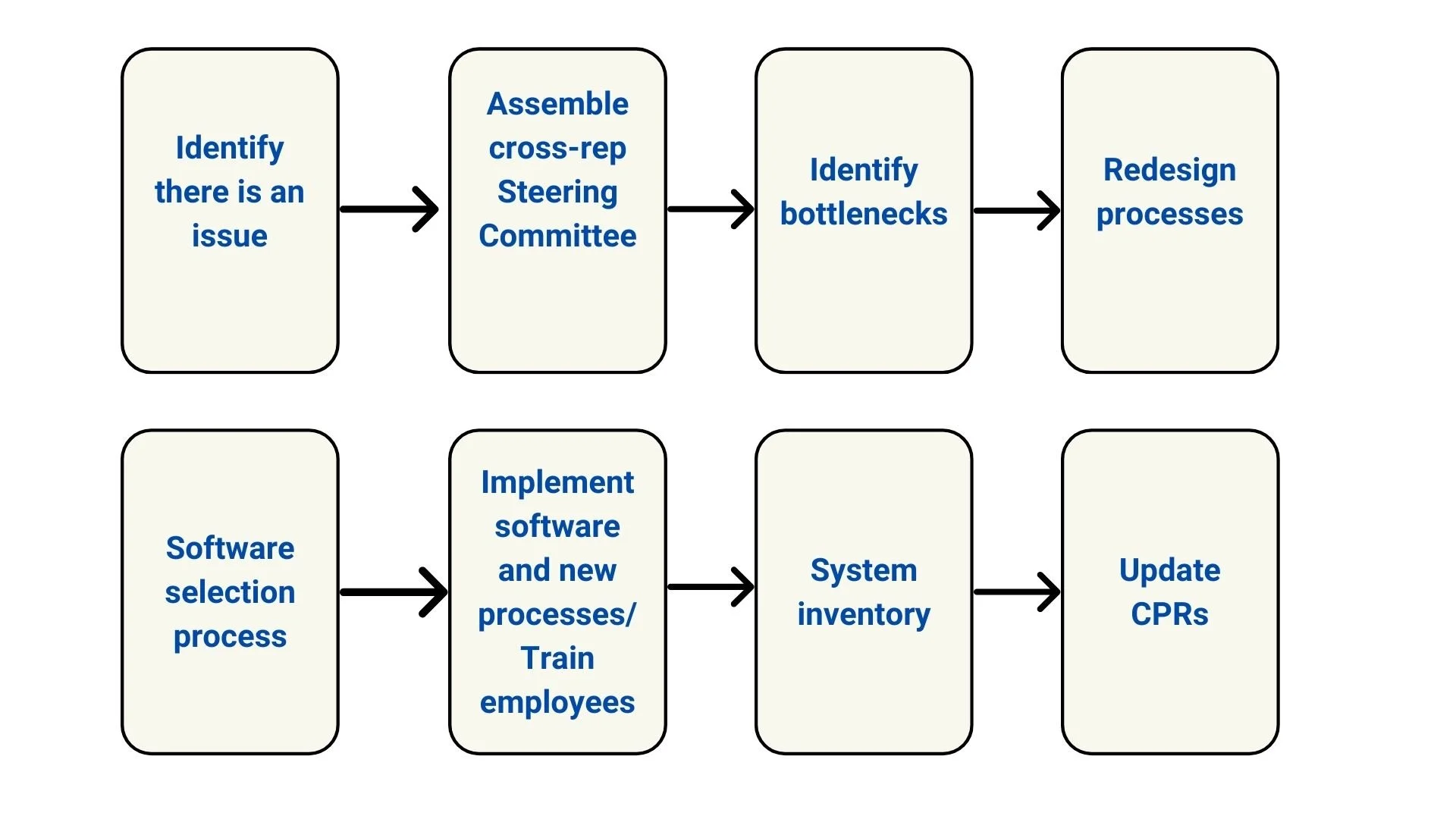

A project and multi-tiered timeline were designed to address the issues. Project steps included:

1. A cross-department Steering Committee was commissioned to oversee the project. Committee members were from construction, engineering, finance, and information technology.

2. Current business process for construction projects were documented for operations and finance. Bottlenecks were identified in current processes.

3. Sample inventories were taken in the field of assets in service. These inventories were compared to maps, GIS, and CPR data. For example, a sample inventory of a section of the utility’s service territory would show 200 50’ poles energized and physically providing service to customers, along with the associated conductor, transformers, and other assets. This total was compared to maps, GIS, and CPR. This was done to get an estimate of the scope of the CPR difference issue.

4. The Steering Committee and consultant held group workshops with personnel from operations and accounting to discuss data needs, bottlenecks, and ways to improve processes.

5. New processes were designed based on an analysis of current processes, incorporating redesigns, and the input from the workshops.

6. The utility issued a detailed request for proposal for software services, with the business processes for construction accounting included along with other utility needs (financial, customer service and billing).

7. Software vendors submitted proposals, gave demonstrations, and the utility selected a provider.

8. The utility undertook a system-wide inventory of its fixed assets. The fixed assets were compared to existing CPRs. The CPR balances were adjusted to reflect actual assets in service.

9. The software was implemented, data was migrated, and the updated CPR information was part of the migration.

10. Detailed policies and procedures manuals were written on processes. The manuals were used as the basis for training programs.

11. Employees were trained in the new business processes.

12. Data flowed into the new system and spot audits were made to determine accuracy. Adjustments were made to processes as identified.

13. Regularly scheduled training continues at intervals to keep employees fresh in the new processes.

While we’re showing these 13 steps above, there are many more steps involved in this project. The project took four years from beginning to end and had a project spend of 7 figures, including consulting, internal training, backfilled internal hours, and software and hardware. This does not include the number of internal hours needed for Steering Committee and other personnel activity hours.

This process is continuous

The description of this project is very high level, and the detail was down in the weeds was quite intense. The utility still considers itself in project mode, making adjustments to processes and testing data as needed. If you ask utility management the key to success, they would point to the disappearance of side-systems and side-records and more reliance on the new software platform’s data and reporting tools.

The reason for this project centered on utility rates and the model needed for operation of service delivery utility of the future. This is not a project to be undertaken likely due to its scope, size, and cost, but a key time to consider a project like this is when your organization plans on changing software or implementing a major software upgrade.

About Russ Hissom - Article Author

Russ Hissom, CPA is a principal of Utility Accounting & Rates Specialists a firm that provides power and utilities rate, expert witness, and consulting services, and online/on-demand courses on accounting, rates, FERC/RUS construction accounting, financial analysis, and business process improvement services. Russ was a partner in a national accounting and consulting firm for 20 years. He works with electric investor-owned and public power utilities, electric cooperatives, broadband providers, and gas, water, and wastewater utilities. His goal is to share industry best practices to help your business perform effectively and efficiently and meet the challenges of the changing power and utilities industry.

Find out more about Utility Accounting & Rates Specialists here, or you can reach Russ at russ.hissom@utilityeducation.com.

The material in this article is for informational purposes only and should not be taken as legal or accounting advice provided by Utility Accounting & Rates Specialists. You should seek formal advice on this topic from your accounting or legal advisor.