The Board's Role in Managing the Utility Bond Rating

It’s easy to manage a bond rating

Hah, this is no joke. A utility’s Board of Directors can definitely influence a bond rating. Utilities finance projects with combinations of cash flow from operations and revenue bond debt. We are now entering an era of rising interest rates, mainly to combat rising inflation. So, the squeeze is on, i.e., debt service will increase due to higher interest rates, and project costs will increase due to inflation. These two occurrences are a negative impact on cash flow. What moves can management and utility Board of Directors make to manage in this environment?

Key Takeaways

The leading bond rating agencies are Moody’s, Standard and Poors, and Fitch.

Managing the bond rating is part of the role of the oversight board of the utility through the approval of budgets and short and long-term strategy.

Enhancing or maintaining the bond rating of a utility is not difficult, but it takes time and attention.

Oversight Utility Boards must take politics out of decisions as much as possible.

The current rising interest rate and inflationary environment will squeeze utility cash flow, and maximizing the utility’s bond rating is one way to counter some of the impacts.

The Board of Director’s role in managing the bond rating

When issuing debt, such as revenue bonds, a utility aims to issue revenue bonds at as low an interest rate as possible. The interest rate of the revenue bond issue is based on the utility’s bond rating, i.e.the, bond rating takes the temperature of a utility’s financial health. In this case, the higher the rating, the lower the interest rate. A lower interest rate means that bondholders pay less for interest expense, providing greater cash flow for the utility.

Bond ratings are provided by the firms Moody’s, Standard and Poors, and Fitch. These three firms are the leading players in providing bond ratings, and a Moody’s rating, a Standard and Poor’s rating, and a Fitch rating all carry equal weight.

One of the most essential jobs of utility management and boards is to manage the utility’s financial structure to maximize its bond rating. Moody’s, Standard and Poors, and Fitch use rating scales to determine the bond rating.

For example, the Moody’s rating scale weights financial ratios to determine the utility’s bond rating. The rating scale heavily weights the debt service coverage ratio, debt to equity ratio, debt to assets ratio, free cash flow, and cash reserves to arrive at its weighting.

Management tools to a better bond rating

Management and the utility board of directors can manage ratios and metrics through budgeting, capital improvement plans, long-range forecasts of future projects, revenue bond debt issued, electric rate increases, and their impacts on cash flows. Some of these tools include:

Focusing on key performance indicators. Since the agencies are focused on the key financial ratios, so should management. Budgets should be developed around cash flows, with emphasis on:

Cash reserves – the bond ratings agencies measure the days of available unrestricted cash, i.e., cash that is not dedicated to debt service or projects. The greater the days of available cash, the higher the rating. Here is the decision grid that is used.

Unrestricted Cash Days on Hand

Utility Accounting and Rates Specialists provides on-line/on-demand courses on operations and construction project accounting, rates, and management for new and experienced co-op and utility professionals and Board Members. Click on the button to see courses that will enhance your career skills and provide value to your organization!

Debt service coverage ratio – this ratio measures the amount of cash available to pay bond principal and interest amounts due. For example, if the utility has $1 of bond principal and interest due, and the utilities cash flow is $1.50, then it has a debt service coverage ratio of 1.5. Cash flow is defined for bond purposes as (Operating revenues - operating expenses + depreciation expense).

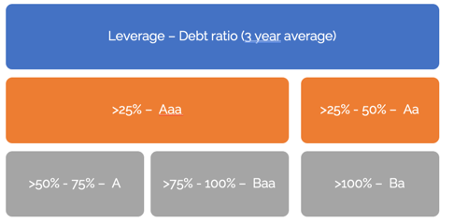

Debt to total assets – Capitalization - This ratio measures the percentage of debt to total assets, an indicator of borrowing capacity. A higher ratio of debt to assets will negatively impact the bond rating. But, as utilities are one of the more solid debt repayment industries, a utility with a high capitalization will find debt opportunities, but at higher interest rates.

Debt capitalization

Strategies to dress up your utility’s financial statements

There are strategies that well-run utilities use that make their financial statements attractive to potential bond buyers and rating agencies. This does not mean that anything untoward or deceptive is going on in the organization. Still, it does mean that management and oversight boards have taken steps to manage finances, and this is reflected in the financials.

Power plant construction

Some solid approaches can include:

1. Rate stabilization reserves - setting aside a “rainy day fund” gives comfort to the ratings agency that funds are available to finance leaner earning years and pay bondholders. Save now and spend later when needed.

2. Long-range forecasting and financing plan over a 15-30 year period - long-term planning shows management’s commitment to implementing and financing long-term strategies.

3. Regular rate increases and the political will of the oversight body to pass needed increases - this shows the understanding of oversight Boards that strategy needs financing and customer rates must cover financing costs.

4. Fallback strategy and mitigation plans for missed budgets - a fallback/mitigation plan is needed when things do not go as planned.

5. Having a defined plan for funding long-term obligations - the aging workforce is driving long-term commitments for pension and post-employment benefits, and customer rates need to support these obligations.

The Board of Director’s role in managing electric rates

Moody’s, Standard and Poor’s, and Fitch emphasize the political environment in increasing electric rates when needed. The Moody’s playbook states that their highest weighted rating is applied to the bond rating formula when:

• “Willingness and ability to recover costs with sound financial metrics.”

o An Aaa weighted rating is applied when the utility has an excellent rate-setting record; rates, fuel, and purchased power cost adjustments are less than 10 days; No political intervention in the past or extremely high support from the related government; Very limited General Fund transfers governed by policy.”

In contrast, Moody’s playbook states their lower weighted rating is applied to the bond rating formula when:

• “Willingness and ability to recover costs with sound financial metrics”

o A Ba rating is applied, when the utility has a consistent record of insufficiently setting rates; Rates, fuel, and purchased power cost adjustments are 100 days or more; Highly political climate or no support from related government; Sizable General Fund transfer not governed by policy”

These examples are the polar extreme of the ratings scale, but one can see that they tell the story of two very different utilities. The commonality in both utilities though is the level of politics in each. As in any industry, although one cannot avoid political concerns, overt politics in the rate and strategy process will not benefit the organization. Governing “by the numbers” is a worthy goal.

Good management practices will translate into solid financials

The article focuses on utilities that are governed at a local, not state, level. Utilities governed at a state level have a much greater complexity of issues to overcome when increasing rates. Nonetheless, the utility’s immediate oversight body must make an effort needed to improve or sustain its bond rating.

While these strategies look attractive to bond ratings agencies, they are also best practices in the industry in sound financial management and addressing the long-term needs of the utility and its customers.

About Russ Hissom - Article Author

Russ Hissom, CPA is a principal of Utility Accounting & Rates Specialists a firm that provides power and utilities rate, expert witness, and consulting services, and online/on-demand courses on accounting, rates, FERC/RUS construction accounting, financial analysis, and business process improvement services. Russ was a partner in a national accounting and consulting firm for 20 years. He works with electric investor-owned and public power utilities, electric cooperatives, broadband providers, and gas, water, and wastewater utilities. His goal is to share industry best practices to help your business perform effectively and efficiently and meet the challenges of the changing power and utilities industry.

Find out more about Utility Accounting & Rates Specialists here, or you can reach Russ at russ.hissom@utilityeducation.com.

The material in this article is for informational purposes only and should not be taken as legal or accounting advice provided by Utility Accounting & Rates Specialists. You should seek formal advice on this topic from your accounting or legal advisor.